69

omnipresence in worldwide highly technologi-

cal markets such as machine building, chemi-

cals, solar energy, automotive supplies and IT

products, as well as their tendency to meet the

characteristics Chinese investors seek in Ger-

man companies: high technical standards, sta-

bility, quality of work, high market shares and a

strong position in Europe and abroad.

54

These

factors indicate that German companies, most

notably Hidden Champions, will continue to be

attractive to Chinese investors for years to

come.

Conclusion

In conclusion, Mergers & Acquisitions can be

considered a complicated and risky business

operation, especially when effectuated bet-

ween companies from two different cultures,

such as those of China and Germany. Howe-

ver, German companies stand to benefit from

Chinese investors’ large volume of investment

capital, strong sales network and local market

access in China. German companies may for

example move non-core production lines to

China to reduce unnecessary costs and con-

centrate more resources towards strengthe-

ning their competences in R&D and technolo-

gical development.

In parallel, with the acquisition of high- valued

European assets through M&As, Chinese com-

panies could speed up their transformation pro-

cess and make up for their weakness in global

brand recognition and core R&D capabilities

55

,

which would otherwise take decades to build

up in a traditional market environment. With the

rapid development of Chinese stock and capital

markets, many Chinese listed and pre-listed

companies are now also showcasing their suc-

cessful acquisitions of European upper-chain

assets in order to improve their chances of a

successful IPO or to quickly increase their mar-

ket capitalization

56

.

With the soaring of their trading price and mar-

ket capitalization, these companies would also

have a stronger ability to raise affordable capi-

tal on the stock market and thus further expand

their business network in the whole global in-

dustry. So there do exist a virtuous cycle and

both acquirer and acquiree could strike for a

not surprising that a large number of invest-

ments of Chinese firms in the past years have

involved German Hidden Champions, more so

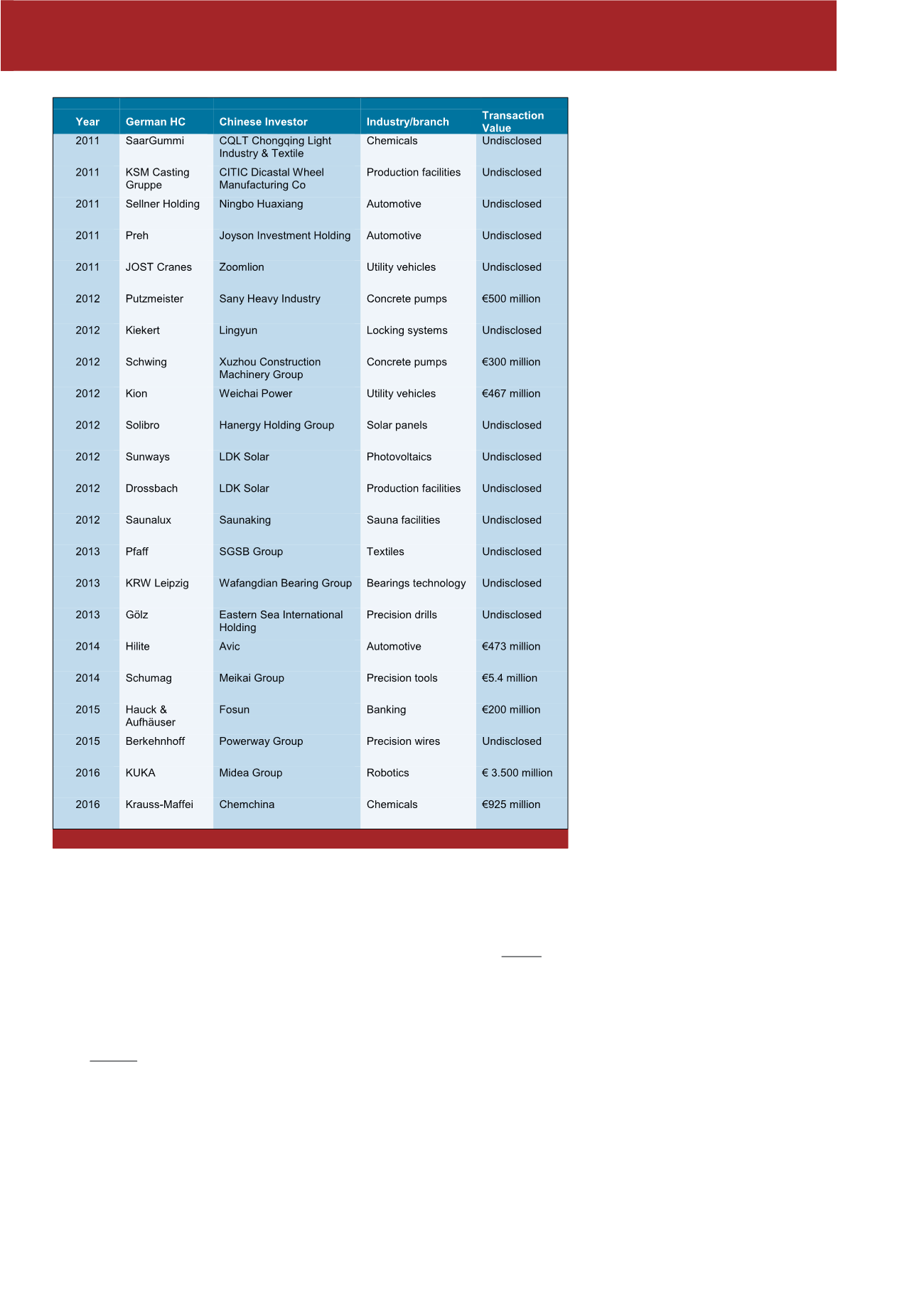

than any other type of company. Table 3 pre-

sents an overview of some of the most recent

publicly-known deals between Chinese inves-

tors and German Hidden Champions.

According to a recent survey by Ernst & Young,

a total of 36 German SMEs were the target of

Chinese investments or purchases in 2015

(also 36 in 2014), maintaining Germany’s posi-

tion of the main target of Chinese investments

in Europe.

53

Unsurprisingly, a large number of

these investments involve German Hidden

Champions. This can be attributed to both their

however, but primarily by the companies’ wish

to be closer to their customers, unlike large

companies which tend to move abroad in low-

wage or low-production cost areas. Even

though the companies operate primarily in Eu-

ropean and North American countries, the

Asian markets are very close, on second

place, in terms of interest and level of invest-

ment. Figure 7 presents an overview of the

main reasons for the Coburg companies’ inte-

rest in internationalizing

51

.

Taking into account the nature of the Hidden

Champions, the sectors in which they operate

and the high standards to which they adhere in

order to remain worldwide market leaders, it is

Table 3: Examples of investments or acquisitions of German HCs by Chinese firms in recent years

52

CM September / Oktober 2018