9

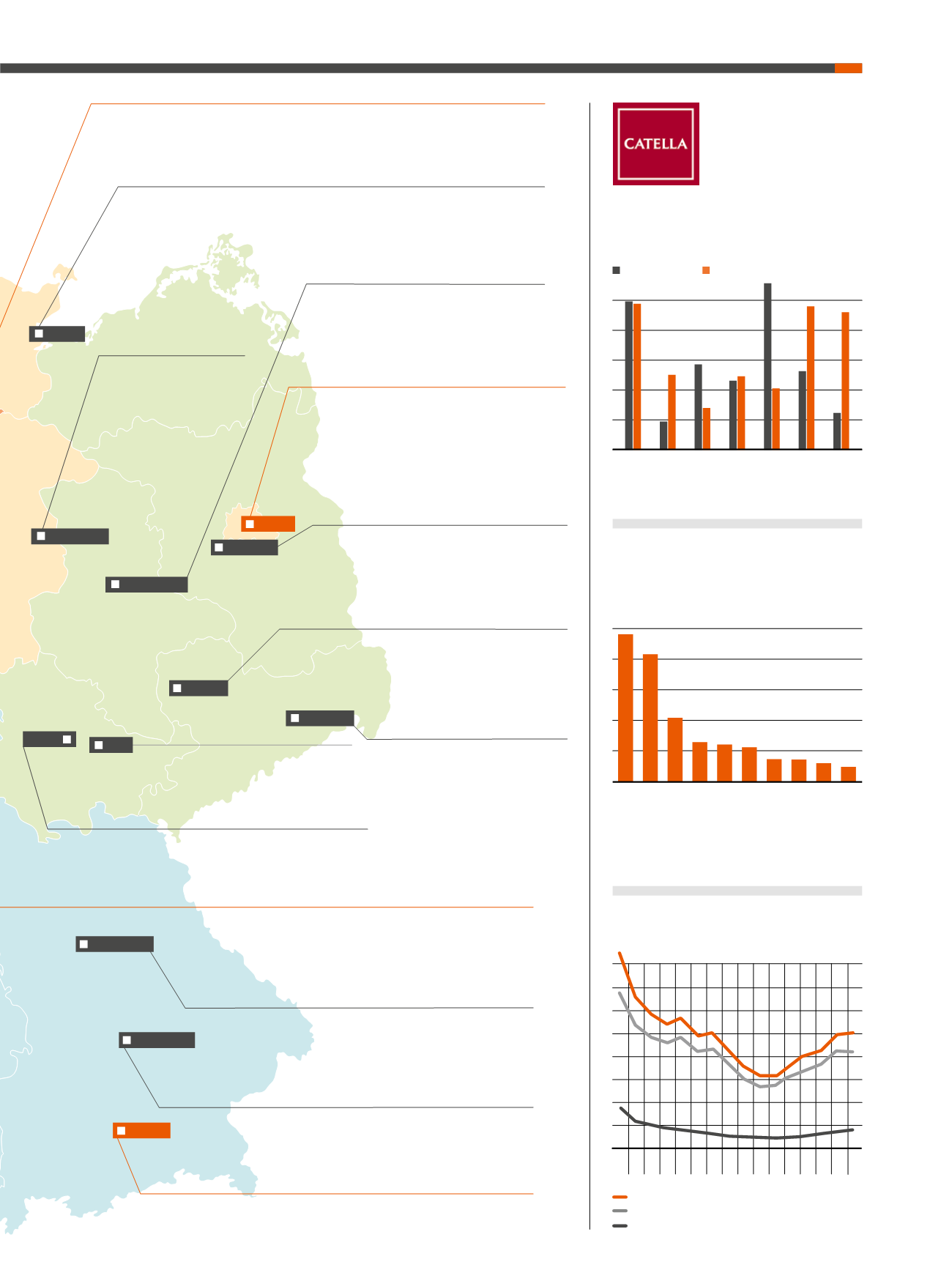

INFOGRAPHIC

Berlin

The residential vacancy rate is currently at approx. 2%, in the

city center under 1%. In the past years not enough residential

space was built in relation to the population growth. Until

2020 every year 20,000 new apartments would have to be

completed to satisfy the demand. In accordance with this, the

rent prices have risen by 30% between 2010 and 2016.

Dresden

The demand for construction is high

and renovations and constructions

have been undertaken for the more

prestigious property owners. The num-

ber of available apartments has

stagnated for a long time, only since

2014 is has sunk through increasing

level of new-builds.

Frankfurt

The target group of project developments are the so called “global

knowledge nomads” and not the local population on average income.

The pressure to move into the cheaper surrounding areas has been

large for years and has further intensified in the recent years.

Hamburg

Only approx. 5% of the new-build apartments are affordable for the average household in

Hamburg. From 2007 until 2012 there was a rent increase (for first-time occupancy) above the

German average of 37%, which led to more people moving to the surrounding areas.

Leipzig

The city has the highest housing stock in relation to

the number of households in Eastern Germany. In 2015

however, rent prices exploded. The locational advantage

existing so far (a large city with enough affordable living

space) seems to be in danger.

Magdeburg

The increase of population in the coming years has

led to a reduction of vacancy rates. In the upper-class

residential segment with waterfront locations beside

the Elbe there is a lot of building activity with projects

and prices comparable to Leipzig or Dresden.

Munich

Until 2030 the city will have a demand for 152,000 new apartments.

Next to the possible construction of skyscrapers there are only two large

new-build areas: in the north-eastern part of the city, east of the S-Bahn

route and in Freiham.

Nuremberg

Rent prices have increased in the last 10 years by 33%. By 2030 there

will be a demand of approx. 23,000 residential units. As a result of this, a

regional residential market between Nuremberg, Erlangen and Fürth will

develop.

Erfurt

Currently all building activity is almost exclusively for affluent inhabitants, for

example for owner-occupied flats either in the center or in the outskirts. The

city is planning 4 ,000 new, affordable rental apartments for the next five years.

NUREMBERG

ERFURT

LEIPZIG

MAGDEBURG

BERLIN

LÜBECK

Wolfsburg

Thanks to the project of the city

to build 6,000 new residential

units by 2020, the idea of “in-

ner-city living” is being enforced.

The current residential projects

make this possible and

consequently a good

infrastructure is

developing.

Potsdam

Potsdam’s residential market is the most dynamic in East

Germany and split between an expensive north and city

center and a less expensive south. There is a lack of apart-

ments, even though there is a lot of building activity. The

housings tock increased from 2008 to 2014 by almost 5%.

POTSDAM

Jena

Jena is on a growth course: in the past years (2008-

2015), 5% more people have moved to the city. In

the past 10 years, the rent prices have increased by

25 %. Meanwhile the rental price brake has taken

form and social housing is a much discussed topic.

MUNICH

Ingolstadt

There is a steady boost in rent price levels. An even stronger increase

was prevented by the fact that there were many investments into living

space from public and private investors. It’s questionable if this trend can

be continued in future, due to the increasing lack of available land.

INGOLSTADT

Lübeck

The residential construction is only slightly expanding, but the large number of planning

permissions granted in recent months can lead to a revitalization of building activities. Water-

front apartments are particularly in demand. In the coming year, an increase of rent prices by

approx. 2 or 3% is expected.

DRESDEN

JENA

WOLFSBURG

Source: Catella Research 2017; As of February 2017; Contact: research@catella.de

2004–2010 2011–2016

TOP 7:

Growth rate of residental net rents –

existing stock, 60-80 SQM

(in %)

25

20

15

10

5

0

Berlin

Cologne

Dusseldorf

Frankfurt

Hamburg

Munich

Stuttgart

TOP 10:

Residential transaction volumes by

federal state in 2016 – single and portfolio

transactions above € 5 Million

(in mnEUR)

Source: Catella Research, RCA

Berlin

North Rhine-

Westphalia

Hesse

Hamburg

Saxony

Bavaria

Saxony-Anhalt

Brandenburg

Baden-

Württemberg

Rhineland-

Palatinate

1,500

1,000

500

0

2,000

2,500

Germany

Former Federal Republic

Eastern states and Berlin

Building completion by units

(in thousands)

350

300

250

200

150

100

50

0

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

400

Source: Destatis