8

GERMANY

ISSUE

I

INFOGRAPHIC

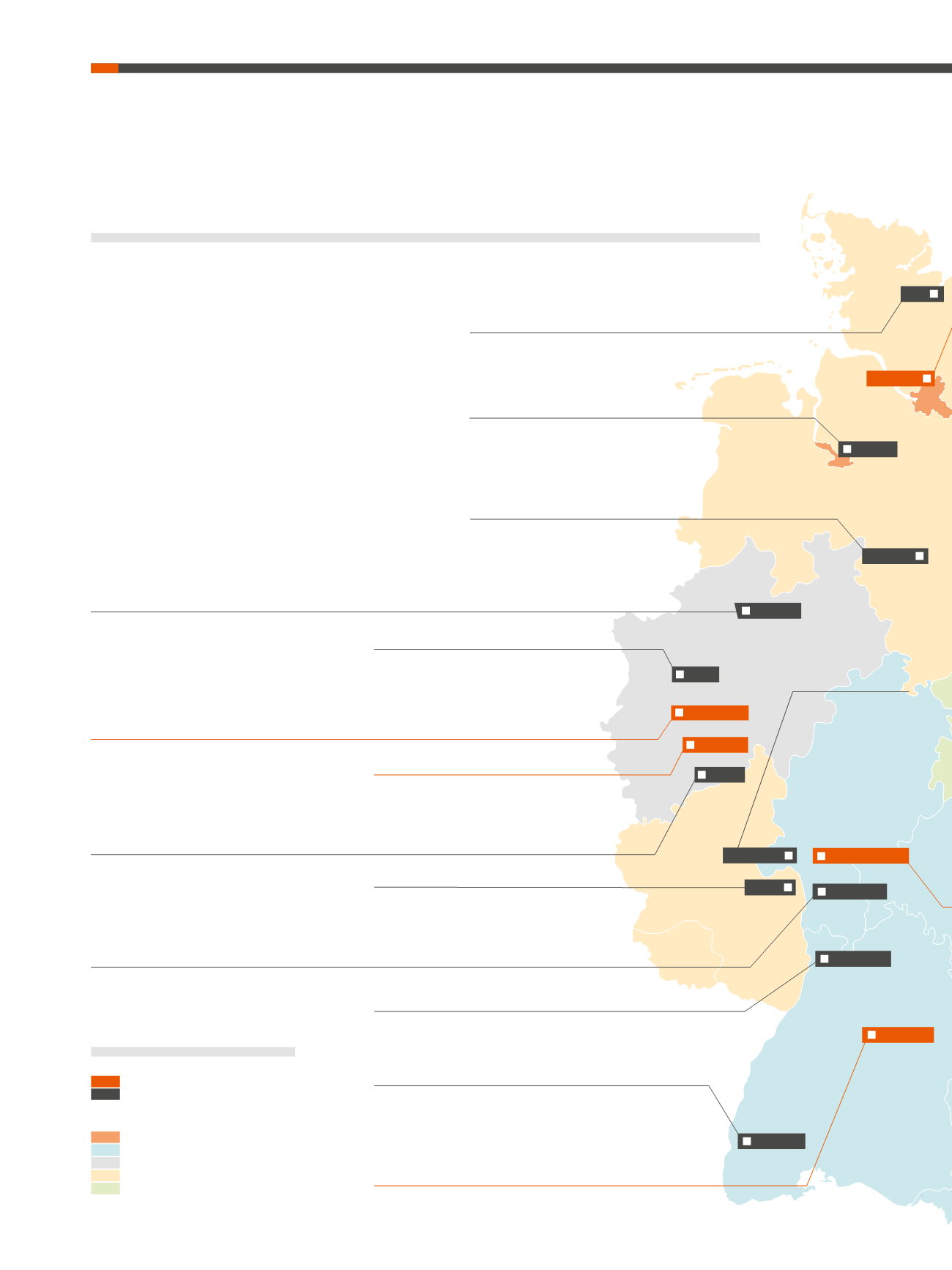

Dusseldorf

Affordable apartments are only located in the outskirts of the

state capital. The average rent price for first-time occupancy

is still slightly increasing. In Dusseldorf there are more luxury

apartments than in the other large German cities, compared

to the number of inhabitants.

Münster

The vacancy rate is quite low and highlights the intense

residential market. Thanks to the strong influx of popu-

lation, the supply of residential space is lower than the

demand. Young families and others, who can’t afford

the central locations, move to the cheaper outskirts or

surrounding areas instead.

Bonn

Affordable living space is missing on the residential

market in Bonn, but the number of new-builds has been

rising for years, although not enough to satisfy demand.

The residential vacancy rate is below 1%. Instead,

people are moving to surrounding areas.

Bremen

Inner-city working-class districts such as Walle are becoming

the focus of the market. This traditional harbour- and

industrial district rapidly became the second most expensive

residential location of Bremen.

Cologne

The number of affordable apartments in the city center has strong-

ly declined in the past years. Consequently, people are moving into

surrounding areas instead. The former industrial and commercial

quarters on the right bank of the Rhine, such as Deutz and Mül-

heim, have achieved the largest rent increases.

Essen

There is a relatively high availability of residential space,

but at the same time quite low public building activity.

The residential market is split, as it is in other cities in the

Ruhr area: poor north and rich south.

Hanover

The amount of completion of residential units in the last 10 years in

Hanover is very low. The consequences are higher price increases and

also an influx into the surrounding areas of Hanover. The average rent

price for first-time occupants has increased from approx. 6.6 €/sqm in

2006 to 9.4 €/sqm in 2016.

Stuttgart

Of the new-build apartments on the market in 2015/2016 only approx. 10% are affordable

for households with an average income. The first residential high-rise building in Stuttgart is

currently being developed in the Europaviertel, while more are in planning .

Heidelberg

The residential property market is intense and in almost all segments there is

excess demand. In the mid-term, the situation should relax due to the construction

of “Bahnstadt” as well as the construction of apartments on conversion areas.

Mainz

The region around Mainz is continuously growing into one market in the

residential sector. The living space situation in Mainz is intense with a vacancy

rate of approx. 1 %. Especially in the more inexpensive segment a lack of

apartments seems to be developing.

Wiesbaden

Two new districts are being

constructed; a further one

is being planned, with

a number of residential

sections in each one. There

are sufficient residential

building areas, but the land

prices are high with a va-

cancy rate of approx. 2%.

BREMEN

HANOVER

ESSEN

DUSSELDORF

COLOGNE

BONN

MAINZ

FRANKFURT/M.

HEIDELBERG

STUTTGART

MÜNSTER

Kiel

Kiel is divided into the expensive western banks – with the city center and University

Campus – and the more inexpensive eastern bank which is close to the city’s indus-

try. It is to be expected that the split of residential locations will grow even further.

HAMBURG

Freiburg

The small amount of new living space developed in the last 10 years was

largely in the upscale segment and has experienced massive price surges.

In order to counteract the lack of apartments – especially in the affordable

segment – the development of new districts will be necessary in future.

FREIBURG

Darmstadt

In the past years, especially multi-storey residential

constructions in the west of Darmstadt were built. The

conversion of former military areas of the US-army opens

up opportunities for residential spaces in prime locations.

DARMSTADT

KIEL

WIESBADEN

Explaining Germany 2017 – Investment

Opportunities in the Residential Sector

Explaining Germany means presenting a multitude of extraordinary facts

that are characteristic of the country, compared to the rest of Europe:

›

Construction activity will accelerate significantly, creating

investment opportunities. Supply across the existing building

stock will remain extremely scarce.

›

Even more stringent regulations in the rental market are expected,

the forthcoming federal election could see housing policy playing

an important role.

›

The phase of fusions and takeovers with residential investors

seems to be calming down – movement can be expected on

the level of property volumes with up to 500 residential units

nevertheless.

›

Looking at the property level, the urge towards serviced

apartments as well as solutions for densifi cation and affordable

housing will further increase. Especially affordable housing will

form a measureable factor on the market this year.

City type

Big 7

Regional Centers

GDP per capita per federal state

Well above average

Above average

Average

Below average

Well below average

German average GDP per capita: 37,853 EUR

Source: Statista 2017